Robot Tellers and the Future of Banking

Editor’s Note: While there’s a big move to mobile banking and contactless payments, customers still prefer visiting their local branch. But in our new retail environment, health and safety must be factored into staff and customer interactions.

This is one reason why robot tellers—considered the future of banking—may not be as far away as we think.

Centerm is combining the best of touchless transactions and streamlined customer service. Its smart banking kiosks, for example, can recognize and interact with clients through facial recognition or a QR code on their smartphone. Personalized banking that once required a teller can now be done at a distance. Read on to learn more.

Consumers find the convenience of mobile banking irresistible. Reviewing account balances, sending money, and even purchasing insurance can be done with a few swipes on a mobile device. This is especially true across Asia, where people are, in effect, carrying their bank around with them everywhere.

China is one example, where in less than a decade, the country has seen a shift from cash to contactless to mobile payments. In 2017 a remarkable $17 trillion in mobile transactions were conducted in China—making the country the world’s biggest mobile payments market.

But even with the popularity of mobile transactions, retail banking is not going away anytime soon. One study shows that consumers prefer branch engagement for more complex services such as loan applications, opening new accounts, and advisory services.

The Agriculture Bank of China, for example, serves 320 million retail customers and 2.7 million corporate clients. At the beginning of 2017, the bank managed 23,682 branches across China.

And now the bank of the future is right around the corner.

Just last summer, a downtown Shanghai branch of China Construction Bank opened the first fully automated bank. “Teller-bots” using facial and voice recognition greet customers. Regular banking services are provided by intelligent teller machines (ITMs), plus online shopping and utility-bill payment services are available. To top it all off, this high-tech bank has a virtual-reality showroom, where visitors can explore potential apartment rentals.

Building the Bank of the Future

To stay competitive, banks must leverage new technologies to deliver the multi-platform, multi-location services customers expect. The Internet of Things, in devices such as thin clients, is playing a big part in delivering these new services and enabling the bank of the future.

Many banks have made a transition from PC platforms running diverse, local applications to a centralized cloud platform. This new system infrastructure has been driven by the need to increase security, ease system management, and reduce operational costs. It’s especially important now, where experienced staff are harder to find, creating the need to offer better services with fewer employees.

The migration to thin-client infrastructure has become a foundation for deploying new technologies. Banking terminals—for both customers and bank personnel—can be purpose-built for specific use cases such as filling out electronic forms or tracking teller transactions. And with the combination of AI, biometric identification, signature recognition, and real-time edge analytics, banks can further expand their services.

From Thin Clients to Smart Banking

This is exactly where Centerm, one of the world’s largest suppliers of thin clients, comes in. The company has deployed hundreds of thousands of systems in financial services and other industries. And now its Smart Banking Solution is enabling financial institutions to offer a smooth and customized experience to its clients.

When customers walk into its branch, they can be greeted by a smart banking kiosk. They can automatically be recognized through biometrics like voice or fingerprint, or log in by scanning a QR code with their smartphone. After logging in, they can execute a wide range of transactions that previously would have required a teller.

For example, customers can fill out electronic forms to open a new account, apply for a loan, make payments, check in for an appointment, and more. This means that before they meet with a loan officer, all the paperwork is complete, digitally signed and even approved. The kiosk might even show a targeted ad, recommending an interesting new product or special offer.

The Benefits of Going Paperless

Bank productivity improves when going from paper workflows to electronic forms. This is especially important for banks challenged by a lack of trained personnel or reduced staffing. And this paperless documentation doesn’t just streamline customer input and business operations—it enables banks to achieve green initiatives.

Many customers—especially the millennial generation—prefer to do most, if not all, of their financial transactions via smartphone. The Centerm solution enables banks to provide the same level of services for mobile customers. Now account holders can conduct transactions, fill out forms online, and digitally sign documents from anywhere in the world.

For both mobile and on-premises banking, all information is captured and encrypted at the edge and forwarded to the bank’s central cloud server. This enables real-time analytics to gain insights on customer transaction history and service preferences. Tellers and other staff can use this information to offer highly personalized service—creating a better customer experience.

In addition, two-way video and audio recordings can be acquired at the counter during teller and client interactions, providing a record of all financial transactions. Archived data is valuable to both the bank and the customer in case of future disputes.

Purpose-Built Terminals with Centralized Management

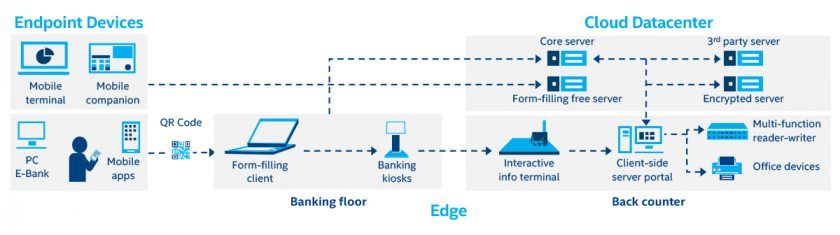

The Smart Banking Solution comprises purpose-built thin clients, intelligent terminals, a cloud-based data center, and a centralized management system. Based on Intel® technology, the end-to-end system enables banks to go well beyond traditional banking—to a digital, paperless system with seamless data flows between client, banking staff, and the data center—with flexible information input options as shown in Figure 1.

Another key benefit of the Centerm thin-client architecture is centralized system management and control. The Centerm Cloud Client Management System (CCCM) provides terminal configuration, deployment, and asset management as well as security control. It is a highly scalable system, with one customer using centralized control for 160,000 Centerm terminals. CCCM functions include:

- Configuration management with automatic discovery, setup, and control

- Deployment management for batch processing, application upgrades, and release notifications

- Safety control for audit monitoring and maintaining a software whitelist

- Asset management with visual reports, plus software and hardware asset statistics

Mobile Banking Gets Personal

Mobile banking is the new normal, yet customers still prefer visiting their local branch. Many transactions are simply easier to accomplish through direct interaction with bank personnel. To be competitive, banks are finding the need to personalize and streamline services, while optimizing their daily operations.

Companies like Centerm provide solutions today that are bringing about the bank of tomorrow. Artificial Intelligence, machine learning, and edge analytics enable a range of secure and convenient services. Customers benefit from convenience and banks benefit with lower costs and new revenue opportunities.